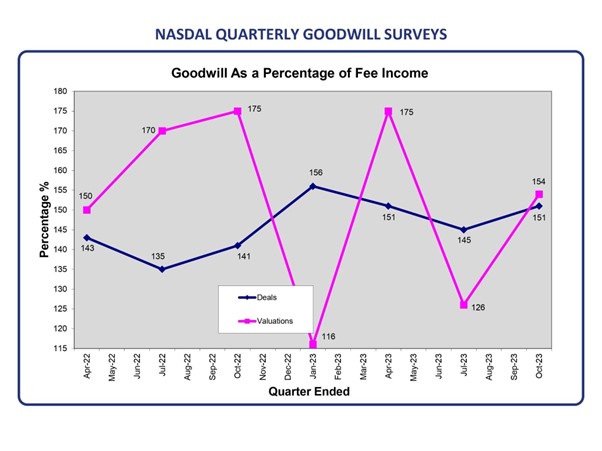

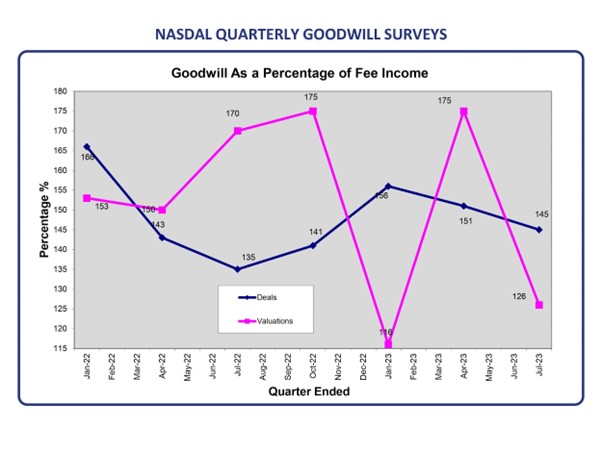

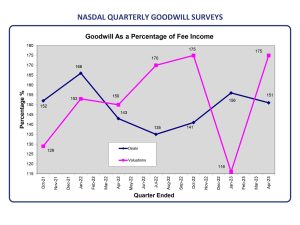

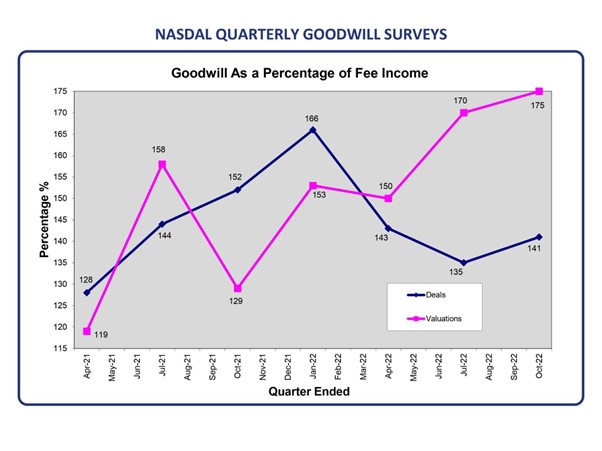

Today has seen NASDAL (National Association of Specialist Dental Accountants and Lawyers) launch its annual Benchmarking Report during a press conference at BDA headquarters in London for the financial period, 2022-23. The eagerly awaited figures have shown:

- Average Associate remuneration is up for the second year in a row from £75,488 to £80,554 – a 6.71% increase

- A small increase in typical practice profits but smaller than inflation (from £172,291 in 2022 to £175,063 in 2023)

- A reduction in private practice profit – a drop from £178,513 in 2022 to £175,800 – but still returning to expected levels (2022 was higher due to the impact of the pandemic)

- Differential of profitability between NHS and Private practices – £17,893

- Practices with Associates still show much higher average net profit per Principal – £181,170 versus £146,843 single-handed in this year’s figures

Ian Simpson, Chartered Accountant and a partner in Humphrey and Co, which conducts the statistical exercise commented, “This year’s figures did fulfil our expectations. We had expected a small rise in practice profits overall and to also see private practices fall back somewhat after the heights of the ‘Zoom Boom’. There is still a big gap in profits between NHS and mixed and private practices and it is difficult to see this gap ever closing as NHS practices cannot pass on increased material and wage costs.

The continued growth of Associates’ income is welcome but likely to be a ‘market correction’ as their incomes have been so static for the last 15 years or so. As we look forward to the 2024 figures, we expect to see a continuation of growth – perhaps across all sectors? It will be an election year and an incoming government may spend more on NHS dentistry. However, we are in a recession so private and mixed practices will have to work hard to grow their businesses whilst keeping costs under control.”

Heidi Marshall, of Dodd & Co, Specialist Dental Accountants and Chair of NASDAL observed, “Thank you to Ian and his team and all the NASDAL members for pooling this useful data. One interesting point to note is that the 2022-23 figures saw a reduction in the number of NHS practices and an increase in the number of mixed and private practices in the sample. Statistical anomaly or change in the market? Time will tell…”

The annual Benchmarking Survey statistics are gathered from the accountant members of NASDAL across the UK who together act for more than a quarter of self-employed dentists. The statistics provide average ‘state-of-the-nation’ figures so NASDAL accountants can benchmark their clients’ earnings and expenditure and help them run their practices more profitably. The basis of the survey figures is 2023 tax returns and accounts with year ends up to 5 April 2023.

Johnny Minford, Commercial and Development Director of DJH Mitten Clarke and NASDAL Media Officer added, “The NASDAL annual profit and loss benchmarking report is a unique and valuable tool which enables NASDAL accountant members to compare their practice owning clients with industry norms. It means that we help our clients really understand what is happening in their dental business.”