Are things looking up in the dental market? Luke Moore Dental Elite

Featured Products Promotional FeaturesPosted by: Dental Design 2nd December 2019

For various reasons – which we needn’t go into here – this is a challenging time for businesses that operate in the UK. Indeed, some sectors have quite a pessimistic view of the future, with projections casting a cloud of concern over many companies in different industries. However, it seems that dentistry may be going its own way.

For various reasons – which we needn’t go into here – this is a challenging time for businesses that operate in the UK. Indeed, some sectors have quite a pessimistic view of the future, with projections casting a cloud of concern over many companies in different industries. However, it seems that dentistry may be going its own way.

It’s good news for dental practice owners as the market has so far remained much healthier than initially expected. Neither stresses on the exchange rate or dental recruitment seem to have slowed the selling and buying of practices, protecting and maintaining goodwill values. If anything, the Dental Elite Benchmarking Survey – Financial Year End March 2020: Interim Update shows a tangible rise in practice values.

Why the uplift?

So, why has the market seemingly taken an upturn, despite the many factors that previously suggested otherwise?

Firstly, we have seen several bolt-on completions following the new private equity investment regarding platform acquisitions of certain dental companies such as Dental Care Group, Portman Dental and Riverdale Healthcare. These are showing no signs of slowing down growth, which is helping to drive the market and retain goodwill values. The extended acquisition footprints of these and other groups are also starting to impact both the regional and national figures. Indeed, we have seen the likes of Mydentist and Colosseum Dental return to the acquisitions market in the past few months as they have completed their mass portfolio management programmes. Further still, the quietly acquisitive Rodericks Dental has grown steadily, helped along by the addition of Denticheck to the group.

Another contributing factor to the growth of the dental market is that most groups have now finished disposing of underperforming practices at lower values. The return to ‘normal’ practice prices has, therefore, given the numbers a bit of a boost as there are far fewer transactions going through to unduly deflate results in some areas of the UK.

All in all, constant movement in the market – supported by increased corporate acquisitions – is proving beneficial for all. Goodwill values are holding strong with demand for businesses in the sector remaining high.

Crunching the numbers

Before we summarise the interim figures for the current financial year so far, a word of caution. These only take into account 6 months of completions, rather than the full 12 months. As such, the number of practice sales included in the results is proportionately smaller and so may demonstrate greater fluctuation in the market than would be apparent with more data.

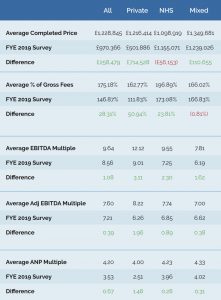

That said, the numbers are definitely encouraging. On average, the completion price for all practices sold through Dental Elite between March and September 2019 increased by more than 28.31 percentiles, which in real world terms is over £250,000. The driving force behind this massive rise has been a significant jump in goodwill values among private practices of more than 50 percentiles. In fact, this is the first time that the value of private practices has surpassed that of NHS practices.

In addition to the potential reasons for this change in the market already discussed, a reduction in the sale of smaller private practices may also have contributed. The current market seems to prefer larger stock where it is exclusively private.

Sale price alone is, of course, only one side of the story. But the Adjusted EBITDA (Earnings Before Interest, Tax, Depreciation and Amortisation) figures show a similarly positive situation. Overall, the Average Adjusted EBITDA values rose by 0.39x, which is staggering in what is an increasingly mature market. Across NHS, mixed and private practices, this accounts for a rise of approximately £60,000 in goodwill value. NHS practices saw a leap of 0.89x for Adjusted EBITDA, confirming a strong position for these businesses despite the figures for percentage of turnover suggesting otherwise. EBITDA per pence of revenue is generally higher in NHS practices than private, as it is driven by a lower renumeration percentage for associates.

National Goodwill Picture

Finally, it seems that the gaps in variations between regions of the UK may be closing slightly. While the London and the South-East continues to enjoy the highest Average Adjusted EBITDA values, Central and Eastern England isn’t far behind. Also, the Average Adjusted Net Profit was highest in Central and Eastern England.

Looking good

In light of the numbers so far, the current financial year is looking good for the dental market. Things can change, of course, and with more data in March we’ll get a more accurate picture of the landscape.

For more information or for your own copy of the latest Dental Elite Benchmarking Survey, visit www.dentalelite.co.uk, email info@dentalelite.co.uk or call 01788 545 900